Section 179 Deduction

When you purchase property or equipment, you utilize these assets over a period of several years (their “useful life”). Depreciation is the process of expensing or deducting the cost over the useful life of the asset rather than the entire amount in the year of purchase.

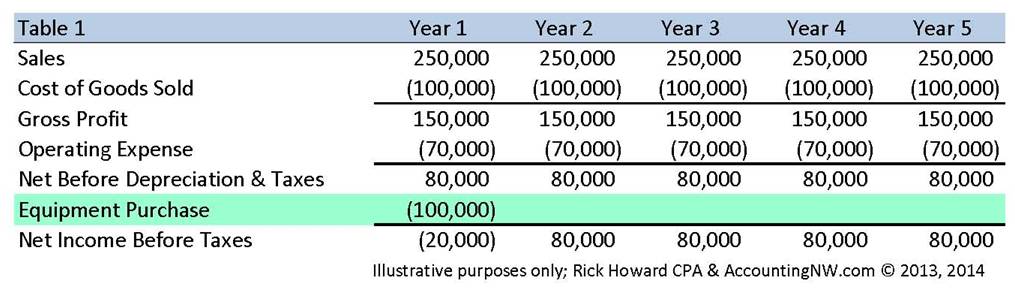

Illustration of business financials information without depreciation:

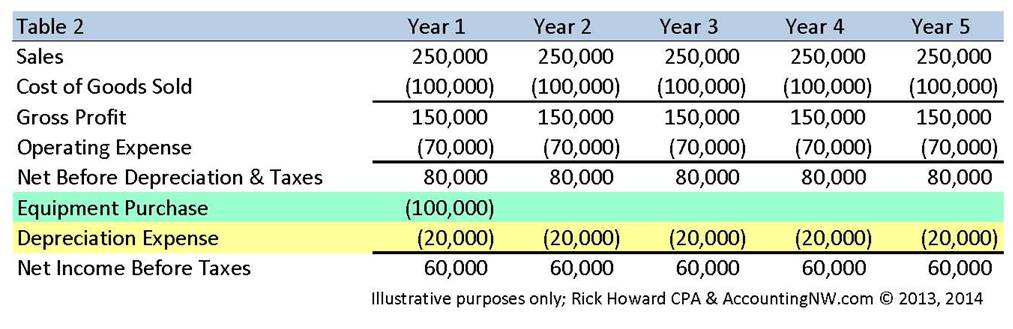

Illustration of business financials information with depreciation:

From an accounting perspective, depreciation provides a more accurate presentation of a business’s financial operations. This is true for tax purposes also, but it also pushes the tax deduction into future years.

SECTION 179 –

Congress passed Section 179 of the tax code to provide incentive for businesses to invest in property and equipment. Section 179 allows businesses to deduct all or part of the purchase price of equipment (up to established “dollar limits”) in the year of purchase. It essentially bypasses depreciation.

Summary of the requirements associated with Section 179:

- There is a maximum “Dollar Limit” allowed ($500,000 in 2013)

- “Investment Limit” whereby the Section 179 deduction is reduced, or “Phased-Out”, after a certain amount ($2,000,000 in 2013)

- Most purchases of new or used tangible personal property qualify (1)

- Allowed only when there is a taxable profit.

- Allowed on assets that are either financed or leased

(1) – See list below of qualifying and non-qualifying property (including examples)

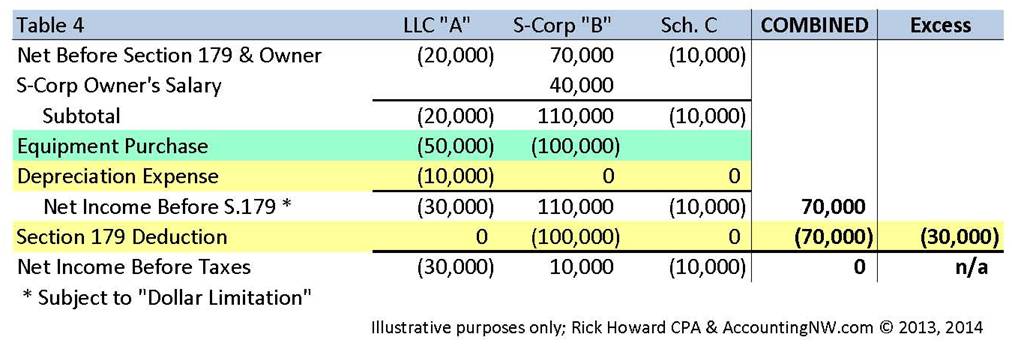

Illustration of business financials information with Section 179 and depreciation:

The rules for Section 179 apply to each entity, including flow-through entities (i.e. Partnership, LLCs, S-Corps). One nuance is that you add the S-Corp owners’ salaries back to the taxable profit to determine the amount of Section 179 deduction allowed. The owner’s share of income and deductions are reported on Schedule K-1 including a separately reported Section 179 deduction. The individual then reports the pass-through entities’ income and deductions on his/her own personal income tax return.

Get help with your planning… Although the basic planning strategy of utilizing Section 179 is fairly easy to understand, individual circumstances can create unexpected results if you aren’t careful. Since the rules for Section 179 apply to each entity, you need to be careful with strategic capital purchases. The rules for Section 179 apply to the entities separately and also to the owner who reports the combined activities.

For example, if Business “A” (an LLC) has a taxable loss but Business “B” (an S Corp) has a taxable profit, equipment purchased in Business B will not be allowed any Section 179 deduction. In a similar way, all your business activity combined is considered at your individual level, so that even if an entity qualifies to take the Section 179 deduction and passes it through to you, if your other business activities off-set part or all of the income from this entity, the Section 179 deduction will not be allowed (note that excess Section 179 deductions will be carried forward to future years).

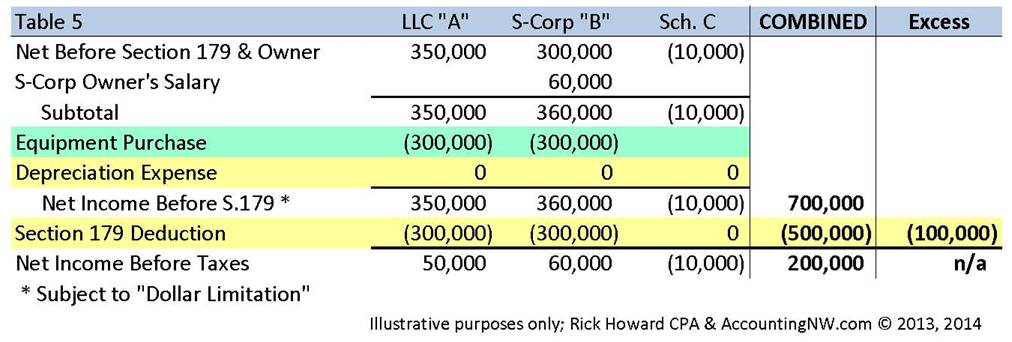

In a similar way, the “Dollar Limitation” applies to each entity, but also to you as the individual. If two pass-through entities allocate Section 179 deductions of $300,000 each to you, your limitation is still $500,000 and you will have $100,000 in excess deduction. This will be a common problem if the law isn’t changed and the dollar limitation is dropped to $25,000 as scheduled for 2014.

BONUS DEPRECIATION –

Bonus depreciation is often used together with Section 179, or when Section 179 is not an option. It can be used when the “Investment Limit” is reached, Section 179 deduction is reduced, or when the Section 179 deduction is limited by the business’ lack of taxable income.

Summary of the requirements associated with Bonus Depreciation:

- Available for only new equipment (software does not qualify)

- Available whether or not there is taxable profit.

Section 179 Qualifying Property:

- Most tangible personal property (i.e. machinery, equipment, furniture)

- Certain other tangible property used for specified purposes

- Single-purpose agricultural or horticultural structures

- Certain storage facilities

- Some examples of qualifying property:

- Agriculture storage facility (e.g., hay, onion, potato, etc.)

- Airplanes & Helicopters

- Automobiles & SUVs (special rules)

- Animals for breeding or dairy (Cattle, Horses, Sheep, etc)

- Orchard trees and Vineyards

- Gas storage tanks

- Greenhouses

- Irrigation Equipment & Water wells.

- Machinery & equipment.

- Office equipment (computers, copiers, printers, etc)

- Office furniture (desks, chairs, cabinets, shelves, etc.)

- Off-the-shelf computer software.

- Oil and gas drilling/well equipment

- Signs

- Trailers

- Trucks

Section 179 Non-Qualifying Property:

- Property held for the production of income (investment property, most rentals).

- Real property, including buildings and their structural components, air conditioning and heating units

- Intangible property (including computer software)

- Property acquired by gift, inheritance or trade, purchased from certain related parties

- Property used outside the United States

- Property used in connection with furnishing lodging

- Property used by a passive activity, tax-exempt organizations, governmental units, foreign persons or entities, or held by an estate or trust

- Some examples of non-qualifying property:

- Air Conditioning & Heating units

- Buildings including Barns, Stables and Warehouses

- Elevators & Escalators

- Foreign used property

- Investment property

- Land

- Landscaping including Shrubbery

- Leased or Rental property

- Outside Improvements including Sidewalks, Fences and Roads

- Swimming pools

Let us help you! The best strategic planning involves looking at all your business activity, and the utilization of both Section 179 and Bonus Depreciation. Please allow us to help you plan to minimize your taxes and get the best value from your capital investment.

Rick

Circular 230 Disclosure: This is to advise you that, unless expressly stated, nothing in this communication (including any attachment or other accompanying materials) was intended or written to be used, and it cannot be used by any taxpayer, for the purpose of avoiding any federal tax penalties, or for promoting, marketing, or recommending a partnership or other entity, investment plan or arrangement to anyone.