Idaho “SALT” Cap Workaround

IDAHO – State And Local Tax (“SALT”) Cap Workaround

Idaho passed legislation allowing for a SALT Cap workaround beginning in the 2021 tax year.

In the past, many taxpayer’s were able to include all of their State and Local Taxes (“SALT”) as an itemized deduction. The Tax Cuts and Jobs Act (TCJA) limited the SALT deduction, capping it at $10,000 beginning in 2018.

The Idaho workaround is for taxpayers with Pass-Through Entities (PTEs) such as partnerships, S-corporations and limited liability companies taxed as either partnerships or S-corporations.

The SALT Cap is a limitation at the individual level; there is no SALT Cap at the business entity level. The workaround allows the business (instead of the individual) to prepay its share of state income tax. The business takes a full deduction on its Federal tax return for these state taxes, reducing the net taxable income that passes through to the individual income tax return.

Note that the state tax is a Federal deduction only. It will be an add-back item on your individual state tax return.

To get the deduction in the current year, the state tax payment needs to be made by year-end.

( Read this post for further background and discussion on the SALT Cap Workaround. )

Idaho specific points:

> Idaho Tax rates: 6.5% of affected business entity (“ABE”) income.

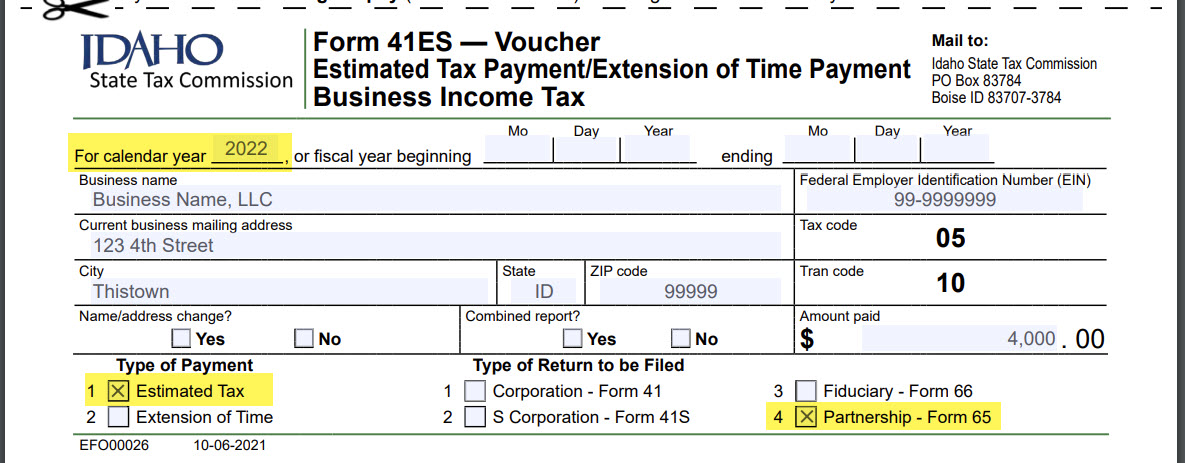

> Use form 41ES “Estimated Tax Payment” voucher with submitted payment.

Example (for entity filing Federal Form 1065 and Idaho Form 65):

Modify the bottom for an entity filing Federal Form 1120-S and Idaho Form 41S:

> Alternatively, you can make your estimated tax payment online at tax.idaho.gov/epay.

The “Quick Pay” option will work well for paying the estimate.