Implementing the $2,500 Expensing Threshold May Not Be Best Practices for Your Business

A capitalization policy is used by a business to set a threshold for determining when a asset purchase should be recorded as a fixed asset (and depreciated), or when the expenditure can be expensed in the current year. The IRS has allowed certain businesses with applicable financial statements with written capitalization policies to establish this threshold at $5,000. For the rest of small businesses, the expensing threshold was set at $500.

A capitalization policy is used by a business to set a threshold for determining when a asset purchase should be recorded as a fixed asset (and depreciated), or when the expenditure can be expensed in the current year. The IRS has allowed certain businesses with applicable financial statements with written capitalization policies to establish this threshold at $5,000. For the rest of small businesses, the expensing threshold was set at $500.

In November 2015, the IRS raised this threshold amount from $500 to $2,500. Tangible asset purchases less than $2,500 can now be posted directly to an expense account, avoiding the process of setting up fixed assets and adding the item to the depreciation schedule.

This may not be a policy you wish to follow.

For most small businesses, Section 179 allows them to accelerate depreciation and expense up to $500,000 of tangible asset purchases in the year they were purchased. If your total tangible asset purchases for a year is $500,000 or less, then there isn’t a tax benefit to applying the higher expensing threshold to your business.

One consideration you should make is the impact of a higher expensing threshold to your financing positioning. Lenders analyze small business’ financial statements and tax returns, and make adjustments to help determine money available for servicing debt.

A national bank posts on its web site that included in its factors for determining loan approval that they take a businesses “net profit, plus its non-cash expenses — depreciation and amortization. Our rule of thumb is that for every $1 in total loan payments, your business must generate $1.50 in cash flow.”

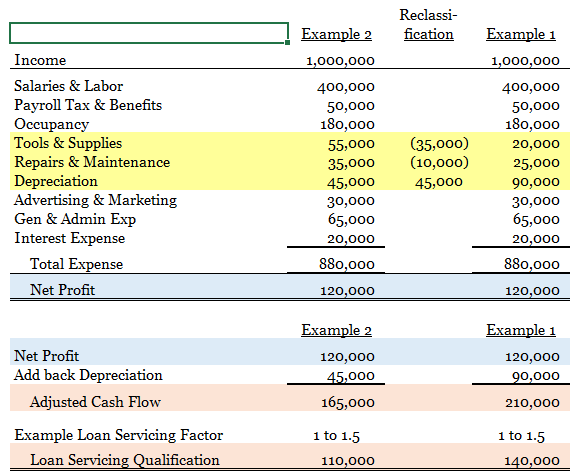

Example 1 – Business had $120k of net profit after depreciation expense of $90k (equipment purchased and depreciated in the same year).

- $ 120,000 Net Profit

- $ 90,000 Depreciation Add-Back

- $210,000 Adjusted Cash Flow

- $ 140,000 Loan servicing qualification amount

Example 2 – Same example as above, however 1/2 of the $90k equipment purchases were from $2,500 or less items and expense while the other 1/2 were larger items (purchased and depreciated in the same year).

- $ 120,000 Net Profit

- $ 45,000 Depreciation Add-Back

- $165,000 Adjusted Cash Flow

- $ 110,000 Loan servicing qualification amount

Explaining it a little differently, but using the same examples above… In Example 2, the business has $35,000 of tangible property purchases under the $2,500 expensing threshold classified into the “Tools & Supplies” account, and another $10,000 of these purchases classified into “Repairs & Maintenance”. While this practice is allowed, and it does simplify the accounting by reducing the additional steps of carrying the items on the depreciation schedule, it also results in a lower adjusted cash flow amount. If these items are reclassified onto the depreciation schedule, Section 179 election will most likely allow us to take the entire deduction in the same year, resulting in the same net profit. What changes is the adjusted cash flow for loan servicing qualification purposes.

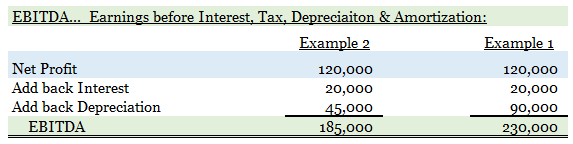

The difference in financial analysis outcomes can also be seen in the computation of EBITDA (earnings before interest, tax, depreciation and amortization) which is a common measure of a company’s operating performance:

While the new threshold may make the accounting for your business more simple, it may not be the best practice.

For Small Businesses: IRS Raises Tangible Property Expensing Threshold to $2,500; Simplifies Filing and Recordkeeping

IR-2015-133, Nov. 24, 2015

WASHINGTON —The Internal Revenue Service today simplified the paperwork and recordkeeping requirements for small businesses by raising from $500 to $2,500 the safe harbor threshold for deducting certain capital items.

The change affects businesses that do not maintain an applicable financial statement (audited financial statement). It applies to amounts spent to acquire, produce or improve tangible property that would normally qualify as a capital item.

The new $2,500 threshold applies to any such item substantiated by an invoice. As a result, small businesses will be able to immediately deduct many expenditures that would otherwise need to be spread over a period of years through annual depreciation deductions.

“We received many thoughtful comments from taxpayers, their representatives and the professional tax community”, said IRS Commissioner John Koskinen. “This important step simplifies taxes for small businesses, easing the recordkeeping and paperwork burden on small business owners and their tax preparers.”

Responding to a February comment request, the IRS received more than 150 letters from businesses and their representatives suggesting an increase in the threshold. Commenters noted that the existing $500 threshold was too low to effectively reduce administrative burden on small business. Moreover, the cost of many commonly expensed items such as tablet-style personal computers, smart phones, and machinery and equipment parts typically surpass the $500 threshold.

As before, businesses can still claim otherwise deductible repair and maintenance costs, even if they exceed the $2,500 threshold.

The new $2,500 threshold takes effect starting with tax year 2016. In addition, the IRS will provide audit protection to eligible businesses by not challenging use of the new $2,500 threshold in tax years prior to 2016.

For taxpayers with an applicable financial statement, the de minimis or small-dollar threshold remains $5,000.